Zubair Yaqoob

Karachi

Despite the political uncertainty imbued by JUI (F)’s Azadi March (protest rally), market took rather positive cue from yesterday’s PIB auction. The yields dropped further, especially in 10yr bond that cemented the view of rate cut in the coming monetary policy.

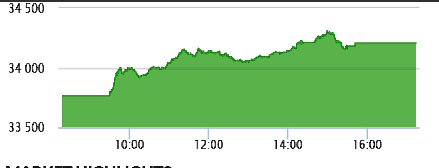

Announcement of next PIB’s auction before the next monetary policy also helped professional money managers take a view that the yields will drop further or atleast maintain, which becomes the reason for reconversion of funds deployed in fixed income back to equities. Buying activity was observed across the board, especially in E&P, Cement and Banking sectors, which kept the stock prices at high level. The index moved uni-directional and made a high of 545pts, closing the session at +442pts. Technology sector realized trading volume of 31.4M shares, followed by Cement (25.1M) and Banks (20.2M). Among scrips, WTL again led the volumes with 24.2M followed by BOP (9.1M) and MLCF (8.5M).

The Index closed at 34,204pts as against 33,761pts showing an increase of 442pts (+1.3% DoD). Sectors contributing to the performance include Banks (+113pts), E&P (+71pts), Fertilizer (+57pts), Cement (54pts) and Inv Banks (+47pts). Volumes increased from 129.9mn shares to 183.9mn shares (+42% DoD). Average traded value also increased by 37% to reach US$ 44.1mn as against US$ 32.2mn.

Stocks that contributed significantly to the volumes include WTL, BOP, MLCF, PPL and STPL, which formed 30% of total volumes.