ZUBAIR YAQOOB

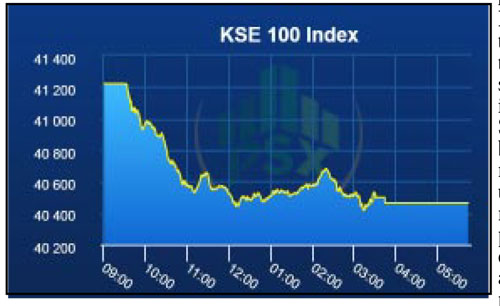

KARACHI The market commenced on a negative note this week with investors resorting to profit-taking. With coalition partners showing dissatisfaction over policies of the PTI-led Govt., lackluster momentum prevailed. Furthermore, concerns over rising inflation kept the sentiment weak. Whereas, overwhelming response to the Treasury Bill Auction (bids over PKR 1.1trn), cushioned the dip. Albeit, the market closed at 43,168 points, (down by 0.1% / 39 points WoW). Sector-wise positive contributions came from Commercial Banks (109pts), Automobile Parts & Accessories (29pts), Automobile Assembler (20pts), Refinery (20pts), and Textile Weaving (12pts). Whereas, negative sector-wise contribution came from Oil & Gas Exploration Companies (96pts) and Power Generation & Distributiontions were led by MEBL (31pts), HBL (28pts), THALL (25pts), BYCO (21pts) and HMB (18pts). Foreign buying continued this week clocking-in at USD 2.8mn compared to a net buy of USD 7.0mn last week. Buying was witnessed in E&Ps (USD 1.4mn) and Fertilizer (USD 1.3mn). On the domestic front, major selling was reported by Insurance Companies (USD 2.8mn) and Individuals (USD 2.2mn). Average Volumes settled at 246mn shares (down by 19% WoW) while average valuetraded clocked-in at USD 49mn (down by 38% WoW). Other major news: HyundaiNishat begins truck production, Govt approves 121 gas schemes, SECP to relax major condition under IPO regulations, International tender floated for auction for 18 new blocks, Car sales plunged by 43.2% during First Half 2019-20, and SBP imposes penalty on five banks. Analysts expect the market to be positive in the upcoming weeks as sentiments should reflect improvement in foreign exchange reserves of the SBP and stable Pak Rupee/USD parity amid inflows in T-bills and narrowing CAD. Albeit, commencement of the financial result season in the coming week will keep certain scrips under limelight. The KSE-100 index is currently trading at a PER of 7.6x (2020) compared to Asia Pac regional average of 12.5x and while offering DY of ~6.3% versus ~2.7% offered by the region.

Friday, April 19, 2024

KSE-100 likely to remain in green during coming weeks

Please login to join discussion

Your source for latest Pakistan, world news. Stay updated on politics, business, sports, lifestyle, CPEC, and breaking news. Accurate, timely, and comprehensive coverage.

Download our Android app for the latest Pakistan and world news in just a tap. Stay informed, anywhere, anytime.