Manama

Islamic financial technology firms, or Islamic fintechs, are moving centre stage in the global Islamic finance industry when it comes to innovation and serving unmet needs in Muslim jurisdictions. These are some of the core finding of the newly-released Global Islamic Fintech Report 2019 produced by UK-based digital finance advisory firm Elipses Group Ltd together with the UK Islamic FinTech Panel, an independent group of Islamic finance and fintech practitioners.

It is only the third annual report on the Islamic fintech industry after previous research on this sector, namely the Islamic FinTech Landscape in 2017 by Islamic business portal IFN and the Islamic FinTech Report 2018 by Islamic advisory DinarStandard.

The new report notes that over the past three years or so, the digital economy has been adapted by Islamic economies and there particularly by Islamic finance, leading to the development of a new segment of financial technology in the industry where innovation is happening.

“Recent developments in financial technology have led to a massive increase in electronic money institutions which have captured much of what was previously the preserve of traditional bricks and mortar banks,” says Harris Irfan, chairman of the UK Islamic FinTech Panel.

“It is therefore inevitable that Islamic fintech firms represent the next wave of growth in the Islamic finance industry,” he adds. The study is based on a survey of 180 companies worldwide, half of them fintechs and the others being incubators and accelerators, consultancies, financial institutions and investors, with respondent being based in the UK, Middle East, other Europe, Southeast Asia, North America and other Asia.

Currently, most of the Islamic fintechs are in their early stages, gearing up to solve challenges of financial inequality, exclusion, underservice or bad customer experience, facing a 1.8bn-people opportunity and growing, the report found. A large part is still in the process of getting regulatory approval and Shariah certification and is in the seeding finance stage.

But the report also notes that progress is quick and 2019 has been a milestone year for Islamic fintechs, with financial intelligence and investing platform IslamicMarkets.com, online halal investment platform Wahed Invest and property crowdfunding platform Yielders all had major funding rounds. In terms of innovation, Indonesian Islamic microfinance fintech Blossom Finance started issuing smart sukuk, while conventional Islamic banks have begun partnering with or creating themselves digital banks such as Meem, ila Bank, CDB Now, Insha and Liv Bank.

Other findings in the report include the perceived growth areas in the Islamic fintech sector. The top five expected growth sectors for 2020 are peer-to-peer and crowd funding, challenger banking, blockchain, robo-advisory and digital personal finance management, as well as online and crowd lending.

However, most Islamic fintechs identified a lack of access to capital as the biggest barrier to growth. Around 70% Islamic fintechs will be seeking to raise equity funding in 2020 with an average round size of $7mn. More mature companies would also pursue other forms of funding namely debt, bridge or mezzanine finance and other forms of funding such as pre-finance in exchange of stocks at a later point of time, the so-called simple agreement for future equity, or SAFE.

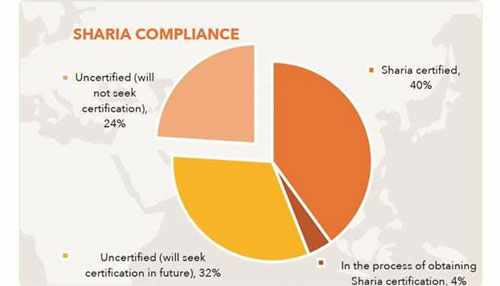

In terms of regulation and certification, 85% of Islamic fintechs have been or are seeking direct or indirect regulated status or expect to be regulated in some form in the near future. Around 76% of Islamic fintechs are already or are expecting to be Shariah-certified, however, whereby 68% felt certification was not necessarily compulsory to be considered Islamic.

The preferred method of market engagement of Islamic fintechs is partnerships, with more institutions expecting to enter such in 2020, the report found. Partnerships are a key growth strategy for Islamic fintechs, with other Islamic fintechs and Islamic banks being the most sought-after partners.

Geographically, Muslim Southeast Asian countries are expected to provide the highest growth potential in 2020 for Islamic fintech, with particularly Indonesia coming into the limelight.

The next strongest growth regions are the Middle East and the UK.

“Ultimately, the winner from all this Islamic fintech innovation ought to be the consumer, both the existing consumer who now has more choice, as well as the previously unserved consumer across the Muslim world,” says Abdul Haseeb Basit, co-founder and principal of Elipses Goup. ”Perhaps most encouragingly, these developments span Southeast Asia, the Middle East, Europe and North America. Islamic fintech is truly a global phenomenon,” he adds. —Gulf Times