Gilly Wright

The strict rules against charging interest and investments deemed contrary to Shariah law earn Islamic finance an understandable reputation for conservatism. But a wider-angle view reveals a different reality. With a youthful, globalized and digitally savvy audience, Islamic financial institutions are rapidly embracing some of the biggest trends in the banking world, notably digital and mobile banking and blockchain technology.

Some of the more restrictive facets of Islamic banking may position these institutions for success. Islamic banks were shielded from the subprime crisis, for example, because complex, high-risk mortgages aren’t Shariah-compliant. Since then, Islamic banks’ ethical approach has helped them grow at twice the speed of conventional banks.

Still, there are concerns that Islamic banking’s circumspect approach has also held back modernization efforts. Standard & Poor’s Global Ratings’ Islamic Finance Outlook 2019 predicts only modest growth this year, and concludes that Islamic banks need both standardization and greater investment in fintech to accelerate growth.

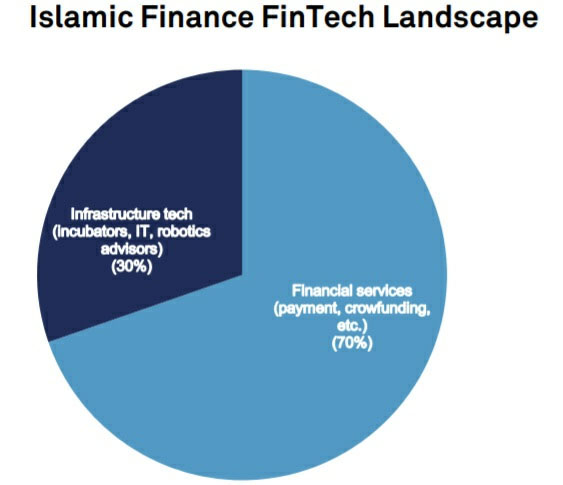

The banks appear to have gotten the message. According to a recent Islamic Fintech Landscape report by Islamic Finance News, there were around 100 Islamic fintech companies at the end of February 2018; 70% were active in financial services, including money transfer, crowdfunding and digital banking; while the remainder focused on technical infrastructure, including IT, artificial intelligence and robotics.

They will soon have company. A 2018 survey of 103 managers by the General Council for Islamic Banks and Financial Institutions (CIBAFI) revealed that 45% were planning to increase or launch digital branches in the future, and 70% viewed fintech and digital transformation as highly or extremely important in strategic decisions.

Kuwait’s Boubyan Bank, for example, recently completed the upgrade of its iMAL Islamic core banking platform in partnership with Path Solutions, an Islamic banking software developer. The upgrade allows Boubyan to enhance its user experience, improve performance and reduce costs. Bringing new products to market and providing valuable customer-data insights will take less time, the bank predicts, helping it provide a more personalized experience.

Launched last year, Qatar Islamic Bank’s (QIB) Instant Finance product is advertised as the fastest and simplest way to obtain personal financing in Qatar; pre-approved customers can get additional personal financing with a few clicks through QIB’s mobile app. Existing customers can get top-up financing instantly, without paperwork and without visiting a branch or talking to a bank representative. Early indications are that QIB’s customers are responding, as Instant Finance contributed 26% of monthly sales to the bank’s flagship retail banking product only five months after its launch.

Instant Finance was the pilot project for a new, agile digital innovation program at QIB, in which a co-located, cross-functional, dedicated team is empowered with decision-making authority to deliver a solution within a strict deadline of 3 1/2 months. Following the success of Instant Finance, QIB is now implementing the agile approach at scale to reengineer all of its key customer-focused products and services.

Abu Dhabi–based ADIB, meanwhile, has resolved an inconvenience associated with Shariah-compliant credit cards: Shariah rules required that customers engage in a new contract to get a new card upon expiration. ADIB developed a renewal process that lets customers renew a card without having to re-sign, and also keep the same card number, so that recurring automated payments are not interrupted. Customers First What all of these initiatives have in common is a focus on improving the customer experience, bringing it up to the standard enjoyed by customers of conventional banks. One of the youngest institutions in Dubai, Noor Bank, adopted Microsoft Dynamics 365’s customer relationship management (CRM) platform last year. It also launched the Noor Trade Biz app, which offers small and medium-sized enterprises (SMEs) discounted services and access to information about third-party financial products. SMEs can also earn and redeem rewards points using the app and track important developments affecting their businesses or investments, according to market and industry trend updates about Noor Business Council events.

Noor has also structured digital platforms to provide Shariah-compliant working-capital finance against accounts receivable. “At Noor Bank, our philosophy has been to address the unmet and unarticulated needs of the client by customizing the solutions to industry and the client,” states Rahul Jayakar, trade head of Global Transaction Services. “Noor Bank’s ability to structure trade solutions and present and implement them in the simplest manner to our clients through various channels is a perfect combination, where traditional, relationship-based banking meets futuristic delivery. And part of our mission is to be recognized as the world’s best contemporary Shariah-compliant bank.”

Upping Innovation Issuance of sukuks—an Islamic financial certificate similar to a bond—fell in the 10 largest markets last year. That, and the recent default and subsequent restructuring by Dana Gas of its sukuk due to lack of Shariah compliance, has underscored the need for standardization. It also encouraged banks to throw more effort into creating genuinely innovative ethical products and services.

Providing sustainable green funding is one such area. Last fall, Jakarta-based CIMB Group acted as bookrunner, lead manager and dealer for a wakala sukuk for the Republic of Indonesia. The deal included a five-year green tranche and a 10-year conventional tranche. The green tranche is the world’s first sovereign green sukuk offering, and the first under Indonesia’s newly established Green Bond and Green Sukuk Framework, whereby proceeds are to be used exclusively for eligible green projects.

CIMB was also, in January 2018, the bookrunner on the first-ever exchangeable trust certificates offering exposure to the Chinese financial sector for Khazanah Nasional Berhad, Malaysia’s sovereign wealth fund. To date, it is also the only equity-linked transaction in the Asia-Pacific region to achieve a sizeable exchange premium at the point of pricing (40%). As Shariah adviser, CIMB structured the deal around an innovative trust certificate, with cash-only settlement, that enabled Khazanah to monetize its holdings in China’s CITIC in a Shariah-compliant manner—the first of its kind in the global markets.

The Khazanah deal highlights the agility that Islamic bankers and Shariah scholars are showing in developing Islamic law that accommodates the disruptive commercial and legal innovations that developments like fintech are likely to stimulate.

For example, S&P sees fintech as a potential threat to business lines such as money transfer, especially in the Gulf region, where expatriates send more than $100 billion back home every year. But fintech can also unlock new avenues for growth and greater financial inclusion. S&P highlights crowdfunding as a potential source of growth in the Islamic world, especially for SME financings and other risky exposures that banks would be too risk-averse to service.

Blockchain may emerge as a facilitator. Smart contracts on a blockchain provide a traceability and transparency that makes them attractive under Shariah law, affording both surety and security. Several Islamic banks are already using or testing blockhain to assist with payments and remittances and for trade finance purposes, including through blockchain Islamic sukuks.

Regtech, too, may solve some of the regulatory and Shariah-compliance barriers that have hindered Islamic finance. A step in this direction is the recent expansion by Dubai International Financial Centre’s fintech hive of its accelerator program for startups to include insurance, Islamic finance and regulatory technological services. Islamic finance faces unique challenges as it integrates into the digital era, but practitioners and regulators alike are determined to make the transition.—(Courtesy: Global Finance)