Islamabad: Thanks to the IMF, as the State Bank of Pakistan (SBP)-held forex reserves increased by $1.1 billion after the International Monetary Fund (IMF) disbursed $1.16 billion under the EFF to Pakistan.

All you need to know about Pakistan, IMF deal

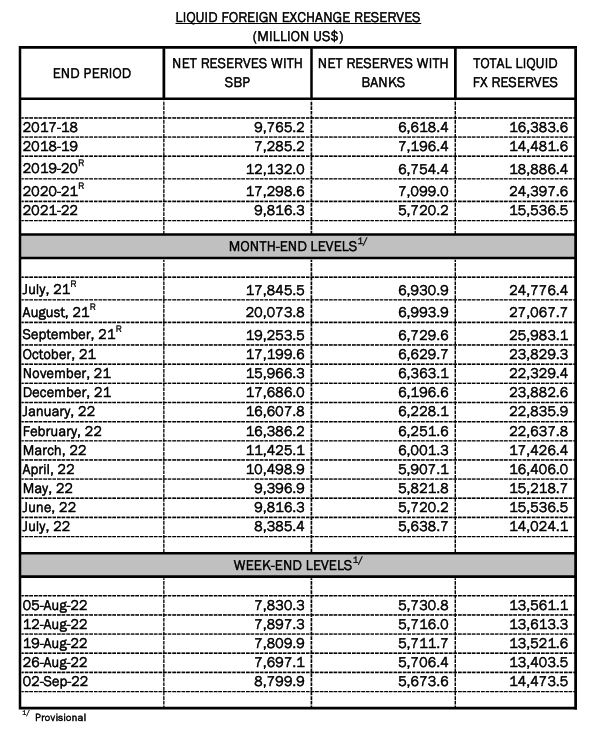

According to a weekly report published on the status of forex reserves by the State Bank of Pakistan, as of September 2, the SBP-held reserves increased by $1.1 billion to reach $8.799 billion from $7.69 billion recorded on August 26.

However, the net reserves held by the commercial banks dropped by $32.8 million to reach $5.67 billion from $5.70 billion recorded a week earlier.

Cumulatively, the total foreign exchange reserves in the country witnessed an increase of $1.07 billion to reach $14.47 billion from $13.4 billion during the period week ended on September 2.

On August 31, the State Bank of Pakistan announced that it received a $1.16 billion loan tranche from the International Monetary Fund (IMF) under the Extended Fund Facility (EFF).

The development came two days after the IMF Executive Board completed the combined 7th and 8th reviews of the loan facility for Pakistan, allowing immediate disbursement of $1.1 billion to the country under the EFF.

Inflation, global conditions will continue to weigh on Pak economy: IMF

The State Bank said that it received proceeds of $1.16 billion (the equivalent of SDR 894 million) after the IMF Executive Board completed the combined seventh and eighth reviews under the Extended Fund Facility (EFF) for Pakistan.

“This will help improve SBP’s foreign exchange reserves and will also facilitate the realization of other planned inflows from multilateral and bilateral sources,” the central bank added.

SBP’s reserves plunge to $7.7 billion; lowest since July 2019