Observer report

Islamabad

Islamic finance is a type of financing activities that must comply with Sharia (Islamic Law). The concept can also refer to the investments that are permissible under Sharia.

The common practices of Islamic finance and banking came into existence along with the foundation of Islam. However, the establishment of formal Islamic finance occurred only in the 20th century. Nowadays, the Islamic finance sector grows at 15%-25% per year, while Islamic financial institutions oversee over $2 trillion.

The main difference between conventional finance and Islamic finance is that some of the practices and principles that are used in the conventional finance are strictly prohibited under Sharia laws.

Principles of Islamic Finance

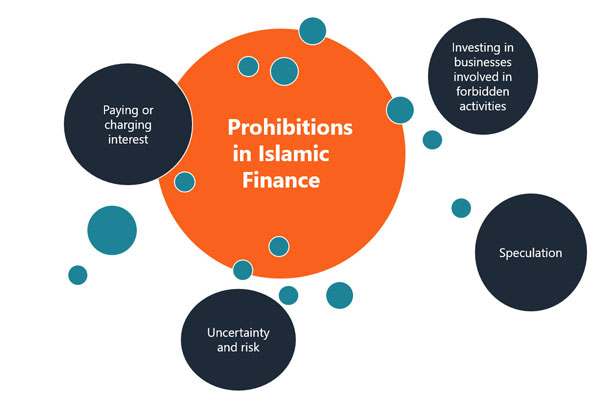

Islamic finance strictly complies with Sharia law. Contemporary Islamic finance is based on a number of prohibitions that are not always illegal in the countries where Islamic financial institutions are operating:

Paying or charging an interest: Islam considers lending with interest payments as an exploitative practice that favors the lender at the expense of the borrower. According to Sharia law, interest is usury (riba), which is strictly prohibited.

Investing in businesses involved in prohibited activities: Some activities, such as producing and selling alcohol or pork, are prohibited in Islam. The activities are considered haram or forbidden. Therefore, investing in such activities is likewise forbidden.

Speculation (maisir): Sharia strictly prohibits any form of speculation or gambling, which is called maisir. Thus, Islamic financial institutions cannot be involved in contracts where the ownership of good depends on an uncertain event in the future.

Uncertainty and risk (gharar): The rules of Islamic finance ban participation in contracts with the excessive risk and/or uncertainty. The term gharar measures the legitimacy of risk or uncertain in nature investments. Gharar is observed with derivative contracts and short-selling, which are forbidden in Islamic finance.

In addition to the above prohibitions, Islamic finance is based on two other crucial principles:

Material finality of the transaction: Each transaction must be related to a real underlying economic transaction.

Profit/loss sharing: Parties entering into the contracts in Islamic finance share profit/loss and risks associated with the transaction. No one can benefit from the transaction more than the other party.

Since Islamic finance is based on several restrictions and principles that do not exist in conventional banking, special types of financing arrangements were developed to comply with the following principles: Profit-and-loss sharing partnership (mudarabah): Mudarabah is a profit-and-loss sharing partnership agreement where one partner (financier or rab-ul mal) provides the capital to another partner (labor provider or mudarib) who is responsible for the management and investment of the capital. The profits are shared between the parties according to a pre-agreed ratio.

Profit-and-loss sharing joint venture (musharakah): Musharakah is a form of a joint venture where all partners contribute capital and share the profit and loss on a pro-rata basis. The major types of these joint ventures are:

Diminishing partnership: This type of venture is commonly used to acquire properties. The bank and investor jointly purchase a property. Subsequently, the bank gradually transfers its portion of equity in the property to the investor in exchange for payments.

Permanent musharkah: This type of joint venture does not have a specific end date and continues operating as long as the participating parties agree to continue operations. Generally, it is used to finance long-term projects.

Leasing (Ijarah): In this type of financing arrangement, the lessor (who must own the property) leases the property to the lessee in exchange for a stream of rental and purchase payments, ending with the transfer of property ownership to the lessee. Investment Vehicles: Due to the number of prohibitions set by Sharia, many conventional investment vehicles such as bonds, options, and derivatives are forbidden in Islamic finance. The two major investment vehicles in Islamic finance.